Housing Market Forecast: What’s Ahead for the 2nd Half of 2024

🏠 As we move into the second half of 2024, here’s what experts say you should expect for home prices, mortgage rates, and home...

Read More

June 24, 2024

As we move into the second half of 2024, here’s what experts say you should expect for home prices, mortgage rates, and home sales.

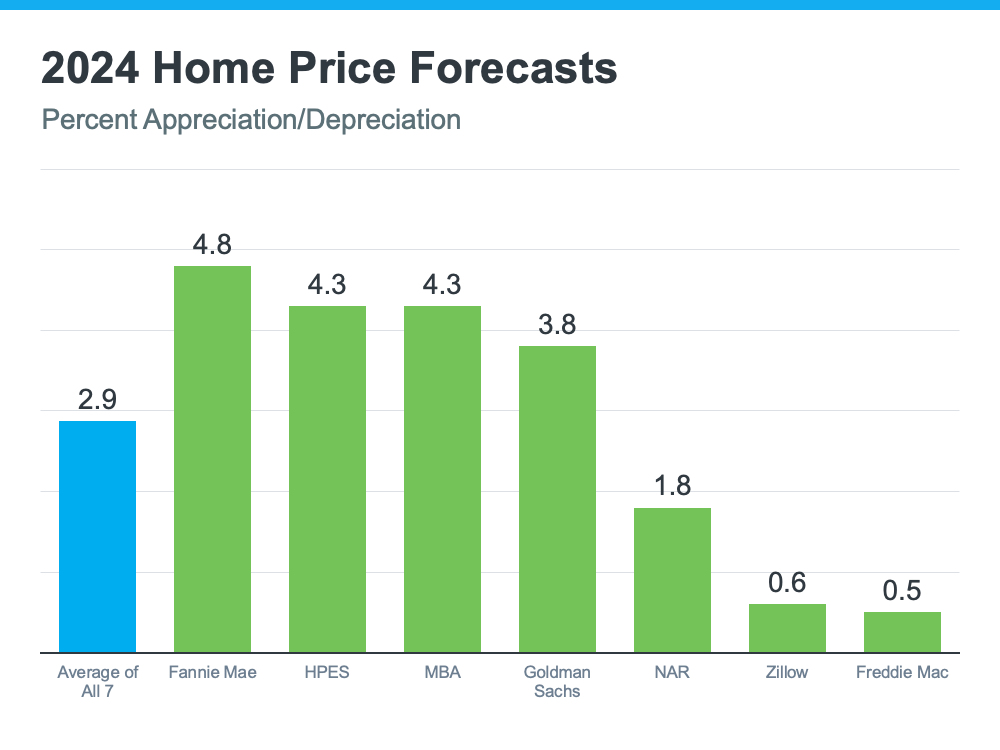

Home prices are forecasted to rise at a more normal pace. The graph below shows the latest forecasts from seven of the most trusted sources in the industry:

The reason for continued appreciation? The supply of homes for sale. Jessica Lautz, Deputy Chief Economist at the National Association of Realtors (NAR), explains:

“One thing that seems to be pretty solid is that home prices are going to continue to go up, and the reason is that we don’t have housing inventory.”

While inventory is up compared to the last couple of years, it’s still low overall. And because there still aren’t enough homes to go around, that’ll keep upward pressure on prices.

If you’re thinking of buying, the good news is you won’t have to deal with prices skyrocketing like they did during the pandemic. Just remember, prices aren’t expected to drop. They’ll continue climbing, just at a slower pace.

So, getting into the market sooner rather than later could still save you money in the long run. Plus, you can feel confident experts say your home will grow in value after you buy it.

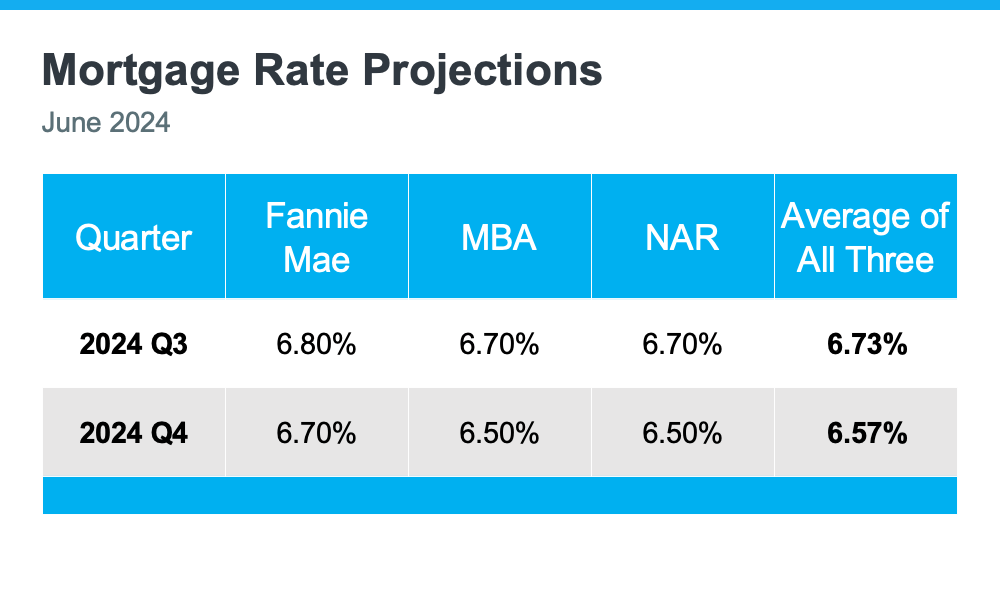

One of the best pieces of news for both buyers and sellers is that mortgage rates are expected to come down a bit, according to Fannie Mae, the Mortgage Bankers Association (MBA), and NAR (see chart below):

When you buy, even a small drop in mortgage rates can make a big difference in your monthly payments. For sellers, lower rates will bring more buyers back into the market, which can help you sell faster and potentially at a higher price. Plus, it may help you get off the fence, if you’ve been hesitant to sell due to today’s rates.

When you buy, even a small drop in mortgage rates can make a big difference in your monthly payments. For sellers, lower rates will bring more buyers back into the market, which can help you sell faster and potentially at a higher price. Plus, it may help you get off the fence, if you’ve been hesitant to sell due to today’s rates.

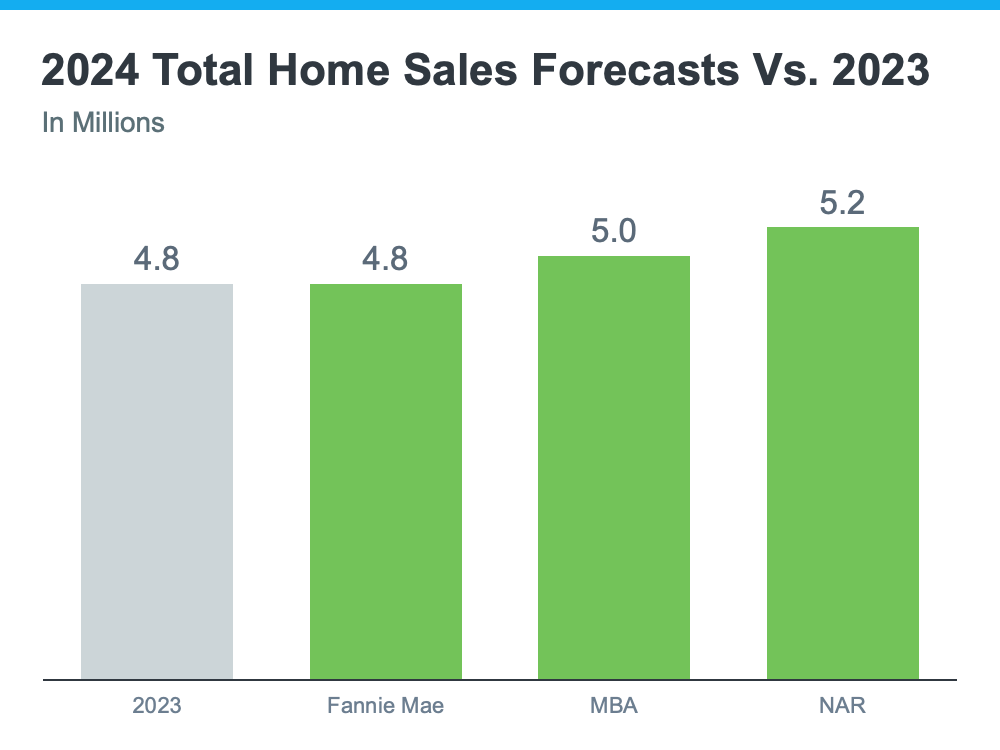

For 2024, the number of home sales will be about the same as last year and may even rise slightly. The graph below compares the 2024 home sales forecasts from Fannie Mae, MBA, and NAR to the 4.8 million homes that sold last year:

The average of the three forecasts is about 5 million sales in 2024 – a small increase from 2023. Lawrence Yun, Chief Economist at NAR, explains why:

“Job gains, steady mortgage rates and the release of inventory from pent-up home sellers will lead to more sales.”

With more inventory available and mortgage rates expected to go down, a few more homes are expected to be sold this year compared to last year. This means more people will be able to move. Let’s work together to make sure you’re one of them.

If you have any questions or need help navigating the market, reach out.

🏠 As we move into the second half of 2024, here’s what experts say you should expect for home prices, mortgage rates, and home...

Read More

June 24, 2024

🏠 You may have heard that there are more brand-new homes available right now than the norm. Today, about one in three homes on...

Read More

June 18, 2024

🏠 Many homeowners looking to sell feel like they’re stuck between a rock and a hard place right now. Today’s mortgage rates are higher...

Read More

June 10, 2024

🏠If you’re planning to move, climate change is something you might want to consider, no matter where you are. Read more….

Read More

May 29, 2024

🏠 If you're thinking of buying or selling a house, it's important to know it doesn't just impact you. Read more….

Read More

May 20, 2024

🏠 If you’re a member of a younger generation, like Gen Z, you may be asking the question: will I ever be able to...

Read More

May 13, 2024

You may have heard that there are more brand-new homes available right now than the norm. Today, about one in three homes on the market are newly built. And if you’re wondering what that means for the housing market and for your own move, here’s what you need to know.

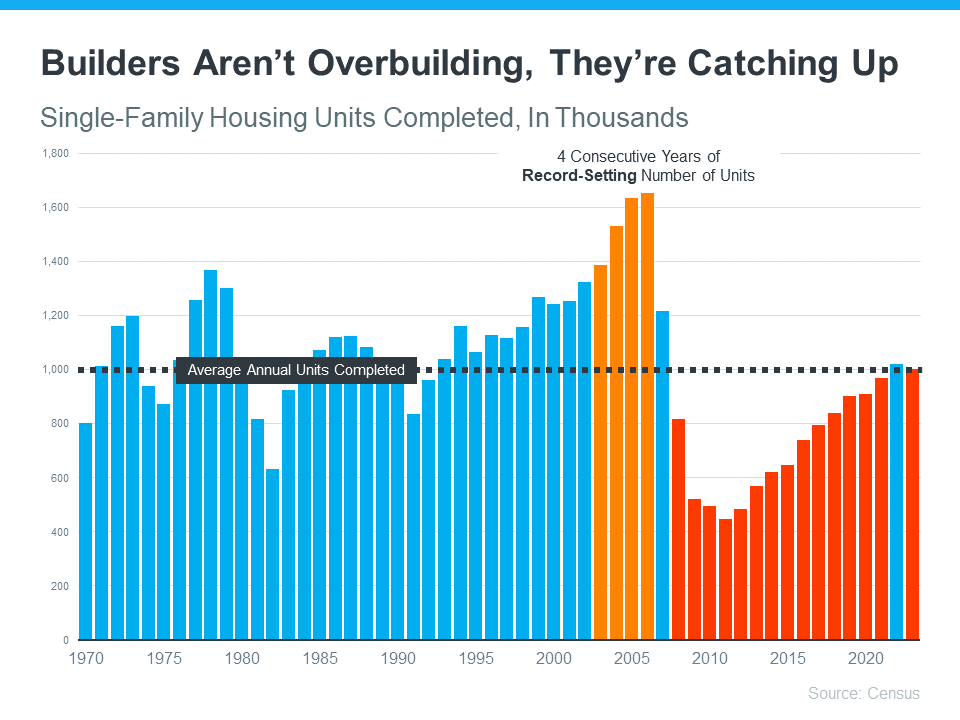

People remember what happened to the housing market back in 2008. And one of the factors that contributed to that crash was that there were too many homes for sale. While only part of the oversupply back then came from builders, the lasting impact is that some people still feel uneasy when they hear new home construction has ramped up.

Even though the supply of new homes has grown this year, the data shows there’s no need to worry. Builders aren’t overbuilding, they’re just catching up.

The graph below uses data from the Census to show the number of new houses built over the last 52 years. Following the crash in 2008, there was a long period of underbuilding (shown in red). And it wasn’t until recently that we finally met the long-term average for how many homes are built in a typical year.

This shows, that even with the increase in new builds we’ve seen lately, there won’t suddenly be an oversupply of homes for sale. There’s too much of a gap to make up after over a decade of underbuilding. And if you’re still worried builders are overdoing it, here’s something else that should be reassuring.

The latest data from the Census on housing starts (homes where builders just broke ground) and permits (homes where builders can start development soon) shows builders are slowing down their pace right now. Why is that?

They’re responding to still high mortgage rates and how those are impacting buyer demand. Basically, they’re pulling back appropriately in response to what’s happening in the market. As an article from HousingWire explains:

“Even with a massive housing shortage across the nation, homebuilders are completing their pipelines and not seeking as many permits to construct new single-family houses.”

Builders remember what happened when they overbuilt in the crash, and they’re looking to avoid a repeat of that. So, they’re being mindful and pulling back a bit.

If you’re considering a newly built home, here’s how this impacts you. With builders seeking fewer permits and not breaking ground on as many new homes, we may be at the peak of new home construction for the year. This doesn’t mean new home construction is screeching to a stop – just that the pace is slowing down now, and that’ll impact what comes to market later this year. As Lawrence Yun, Chief Economist at the National Association of Realtors (NAR), says:

“Given the recent declines in housing starts, home completions will steadily show declines in about six months.”

So, if you’re ready and able to buy now, you may find you’ll have more newly built options to choose from now versus later on. This may be enough reason to kick off your search.

Just be sure to work with a local real estate agent you know and trust throughout the process. An agent will have valuable insight into builder reputations and other key factors specific to your market. And if there isn’t much new construction near you, they’ll be able to point you toward a nearby area where there is.

While it’s true new home construction is a bigger segment of the market than the norm, that’s not a bad thing. Builders aren’t overbuilding, and they’re responding to market signals to avoid repeating the mistakes that were made in 2008.

🏠 You may have heard that there are more brand-new homes available right now than the norm. Today, about one in three homes on…

Read More

June 18, 2024

🏠 Many homeowners looking to sell feel like they’re stuck between a rock and a hard place right now. Today’s mortgage rates are higher…

Read More

June 10, 2024

🏠If you’re planning to move, climate change is something you might want to consider, no matter where you are. Read more….

Read More

May 29, 2024

🏠 If you’re thinking of buying or selling a house, it’s important to know it doesn’t just impact you. Read more….

Read More

May 20, 2024

🏠 If you’re a member of a younger generation, like Gen Z, you may be asking the question: will I ever be able to…

Read More

May 13, 2024

🏠 Thinking about selling your house? As you make your decision, consider what’s pushing you to think about moving Read more…

Read More

May 7, 2024

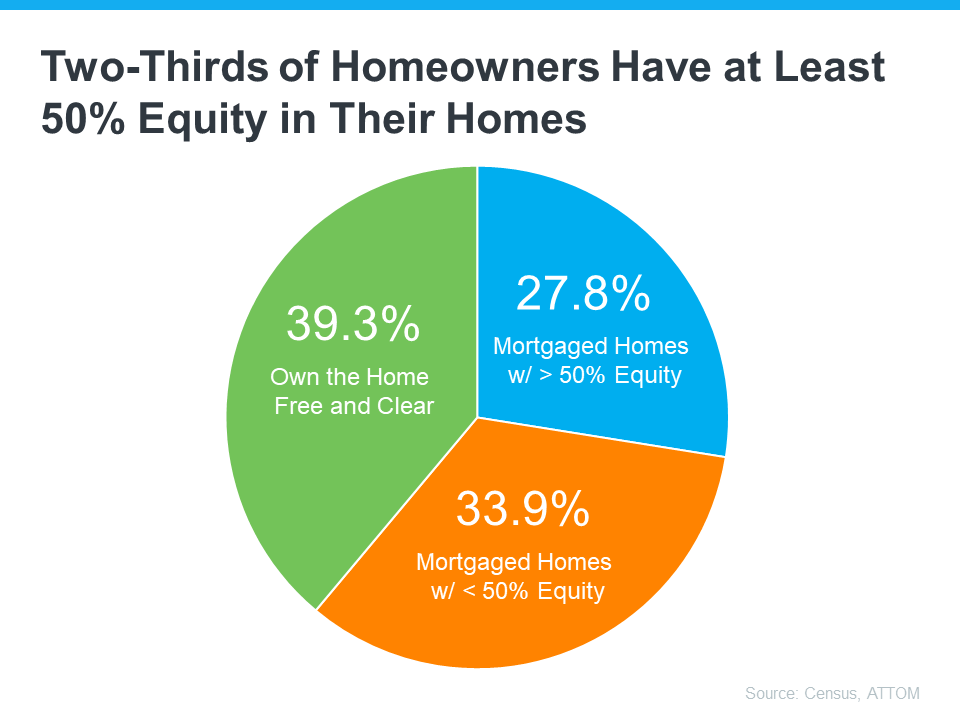

Many homeowners looking to sell feel like they’re stuck between a rock and a hard place right now. Today’s mortgage rates are higher than the one they currently have on their home, and that’s making it harder to want to sell and make a move. Maybe you’re in the same boat.

But what if there was a way to offset these higher borrowing costs? There is. And the money you need probably already exists in your current home in the form of equity.

Think of equity as a simple math equation. Freddie Mac explains:

“. . . your home’s equity is the difference between how much your home is worth and how much you owe on your mortgage.”

Your equity grows as you pay down your loan over time and as home prices climb. And thanks to the rapid home price appreciation we saw in recent years, you probably have a whole lot more of it than you realize.

The latest from the Census and ATTOM shows more than two out of three homeowners have either completely paid off their mortgages (shown in green in the chart below) or have at least 50% equity (shown in blue in the chart below):

That means the majority of homeowners have a game-changing amount of equity right now.

After you sell your house, that equity can help you move without worrying as much about today’s mortgage rates. As Danielle Hale, Chief Economist for Realtor.com says:

“A consideration today’s homeowners should review is what their home equity picture looks like. With the typical home listing price up 40% from just five years ago, many home sellers are sitting on a healthy equity cushion. This means they are likely to walk away from a home sale with proceeds that they can use to offset the amount of borrowing needed for their next home purchase.”

To give you some examples, here are a few ways you can use equity to buy your next home:

Want to find out how much equity you have? To do that, you’ll need two things:

You can probably find the mortgage balance on your monthly mortgage statement. To understand the current market value of your house, you can pay hundreds of dollars for an appraisal, or you can contact a local real estate agent who will be able to present to you, at no charge, a professional equity assessment report (PEAR).

Once you’ve connected with a trusted local agent and run the numbers, you’re one step closer to making a move you may not have thought was realistic – all thanks to your equity.

If you want to find out how much equity you have and talk more about how it can make your next move possible, let’s connect.

🏠 Many homeowners looking to sell feel like they’re stuck between a rock and a hard place right now. Today’s mortgage rates are higher…

Read More

June 10, 2024

🏠If you’re planning to move, climate change is something you might want to consider, no matter where you are. Read more….

Read More

May 29, 2024

🏠 If you’re thinking of buying or selling a house, it’s important to know it doesn’t just impact you. Read more….

Read More

May 20, 2024

🏠 If you’re a member of a younger generation, like Gen Z, you may be asking the question: will I ever be able to…

Read More

May 13, 2024

🏠 Thinking about selling your house? As you make your decision, consider what’s pushing you to think about moving Read more…

Read More

May 7, 2024

🏠 Thinking about selling your house? If you are, you might be weighing factors like today’s mortgageRead more…

Read More

April 29, 2024

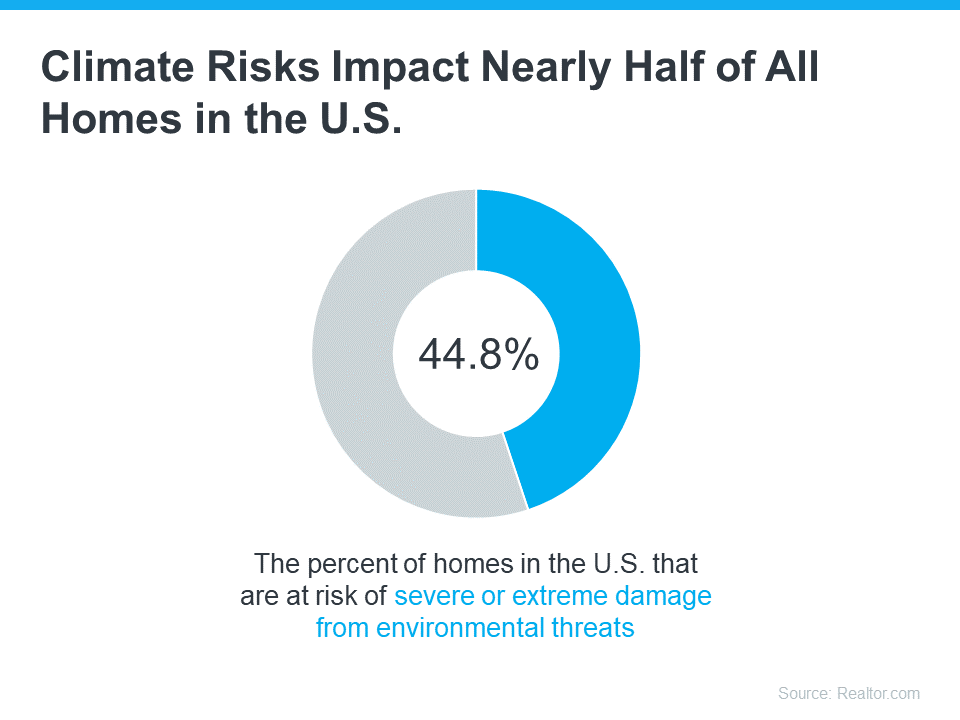

Climate change is impacting where people buy homes. As the experts at the National Association of Realtors (NAR) explain:

“Sixty-three percent of people who have moved since the pandemic began say they believe climate change is—or will be—an issue in the place they currently live.”

If you’re planning to move, climate change is something you might want to consider, no matter where you are. A recent study from Realtor.com helps put the growing impact climate change is having on real estate into perspective (see below):

So, how can you be sure your investment is safe from the elements?

For starters, work with a local real estate agent to understand the likelihood of your future home being exposed to hazards like wind, floods, and wildfires. Your agent will know the area and be able to tell you about the risks you’ll most likely face.

Beyond that, there are two important factors to think about: the quality of the home you want to buy and the insurance you’ll need to protect it.

If you’re planning to be in your home for many years, you want to know it’s going to last. One way to think ahead is to work with your real estate agent to ensure the home you buy can withstand environmental hazards. They’re up to date on the most common building and remodeling techniques—like a secondary water barrier on the roof or noncombustible, fire-resistant exterior walls—used to protect homes from the effects of climate change.

And if the home you’re interested in doesn’t have the features you’re looking for, they can help you determine what you may be able to negotiate in the contract or what work it might require in the future.

Once you’re confident the home you’re looking at is well built, the next step is finding out what it’s going to take to insure it. As Selma Hepp, Chief Economist at CoreLogic, says:

“. . . homeowners are going to become increasingly more aware of risks of living in some areas as it becomes prohibitively expensive or very difficult to obtain hazard insurance.”

In areas where climate risks are having a bigger impact, the right home insurance can make a big difference. And the price of that insurance is an important factor when thinking about your budget and the true cost of buying and protecting your home. Get an insurance quote early in the process because you may want to compare multiple quotes and it can take several weeks to get them.

While this may feel like a lot to consider, don’t worry. An agent can help. Your real estate agent will be your go-to resource on the homebuying process, what to look for and consider, and how climate change may affect your next home. With the right planning and an agent’s expert advice, you can make this happen. Homeownership is worth it. And with a great agent by your side, you can make sure the home you find is the right fit.

Climate change is an important factor to think about when buying a home. After all, your home is a huge investment, and you want to be ready for anything that might affect it. Let’s chat so you can find the perfect home.

🏠If you’re planning to move, climate change is something you might want to consider, no matter where you are. Read more….

🏠 If you’re thinking of buying or selling a house, it’s important to know it doesn’t just impact you. Read more….

🏠 If you’re a member of a younger generation, like Gen Z, you may be asking the question: will I ever be able to…

🏠 Thinking about selling your house? As you make your decision, consider what’s pushing you to think about moving Read more…

🏠 Thinking about selling your house? If you are, you might be weighing factors like today’s mortgageRead more…

🏠 Over the past year, many have discussed the challenge of buying a home. While affordability remains Read more…

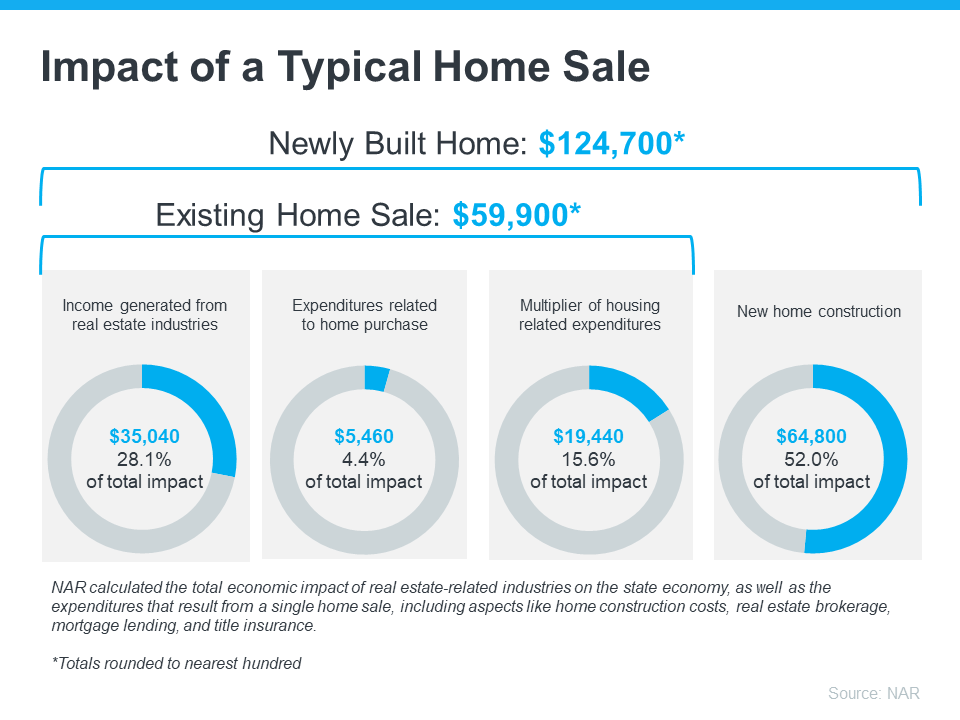

If you’re thinking of buying or selling a house, it’s important to know it doesn’t just impact you—it helps out the local economy and your community, too.

Every year, the National Association of Realtors (NAR) puts out a report that breaks down the financial impact that comes from people buying and selling homes (see visual below):

When a house is sold, it really boosts the local economy. That’s because of all the people needed to build, fix up, and sell homes. Robert Dietz, Chief Economist at the National Association of Home Builders (NAHB), explains how the housing industry adds jobs to a community:

“. . . housing is a significant job creator. In fact, for every single-family home built, enough economic activity is generated to sustain three full-time jobs for a year . . .”

It makes sense that housing creates a lot of jobs because so many different kinds of work are involved in the industry.

Think about all the people involved with selling a house—city officials, contractors, lawyers, real estate agents, specialists, etc. Everyone has a job to do to make your deal go through. So, each transaction is a big help to those who work and live in your community.

Put simply, when you buy or sell a home, you’re helping out your neighbors. So, when you decide to move, you’re not just meeting your own needs—you’re also doing something good for your community. Just knowing your move helps so many people around you can give you a sense of empowerment as you make your decision this year.

Every time a home is sold, it really helps out the local economy. If you’re ready to move, let’s get in touch. It won’t just change your life—it’ll also do a lot of good for the whole community.

🏠 If you’re thinking of buying or selling a house, it’s important to know it doesn’t just impact you. Read more….

🏠 If you’re a member of a younger generation, like Gen Z, you may be asking the question: will I ever be able to…

🏠 Thinking about selling your house? As you make your decision, consider what’s pushing you to think about moving Read more…

🏠 Thinking about selling your house? If you are, you might be weighing factors like today’s mortgageRead more…

🏠 Over the past year, many have discussed the challenge of buying a home. While affordability remains Read more…

🏠 Expenses involved in buying a home, from the down payment to closing costs. But did you know your tax refund can Read more…

If you’re a member of a younger generation, like Gen Z, you may be asking the question: will I ever be able to buy a home? And chances are, you’re worried that’s not going to be in the cards with inflation, rising home prices, mortgage rates, and more seemingly stacked against you.

While there’s no arguing this housing market is challenging for first-time homebuyers, it is still achievable, especially if you have professionals on your side.

Here are some helpful tips you may get from a pro.

If a down payment is your #1 hurdle, you may have options to give your savings a boost. There are over 2,000 down payment assistance programs designed to make homeownership more achievable. And, that’s not the only place you may be able to get a helping hand. While it may not be an option for everyone, 49% of Gen Z homebuyers got money from loved ones that they used toward a down payment, according to LendingTree.

And chances are you won’t need to put 20% down (unless specified by your loan type or lender). So be sure to work with a trusted mortgage professional to explore your options, find out how much you’ll really need, and learn about any guidelines on getting a gift from loved ones.

Another thing a number of Gen Z buyers are doing is ditching their rental and moving back in with friends or family. This can help cut down your housing costs so you can build your savings a whole lot faster. As Bankrate explains:

“. . . many have opted to stop renting and live with family in order to boost their savings. Thirty percent of Gen Z homebuyers move directly from their family member’s home to a home of their own, according to NAR.”

When you’ve saved up enough, here’s how a pro will help you approach your search. Since the supply of homes for sale is still low and affordability is tight, they’ll give you strategies and avenues you may not have considered to open up your pool of options.

For example, it’s usually more affordable if you consider a rural or suburban area versus an urban one. So, while the city may be livelier and more energetic, the cost of living may be reason enough to look at something further out. And if you consider smaller homes and condos or townhouses, you’ll give yourself even more ways to break into the market. As Colby Stout, Research Analyst at Bright MLS, explains:

“Being flexible on the types of home (e.g., a condo or townhome versus a single-family home) and exploring more affordable neighborhoods is important for first-time buyers.”

And lastly, an agent can help you really think about your must-have’s and nice-to-have’s. Remember, your first home doesn’t have to be your forever home. You just need to get your foot in the door to start building equity. If you want to buy, you may find making some compromises is worth it. As Chase says:

“An open-minded approach to house-hunting may be one way for Gen Z homebuyers to maintain some edge. This could mean buying in areas that are less expensive. Differentiating needs vs. wants may help in this area as well.”

An agent will help you prioritize your list of home features and find houses that can deliver on the top ones. And they’ll be able to explain how equity can benefit you in the long run and make it possible to move into that dream home down the line.

Real estate professionals have expertise on what’s working for other buyers like you. Lean on them for tips and advice along the way. As Directors Mortgage says, with that support you can make it happen:

“The path to homeownership may not be a straightforward one for Gen Z, but it’s undoubtedly within reach. By adopting the right strategies, like exploring down payment assistance programs and sharing living costs with relatives, you can bring your dream of owning a home closer to reality.”

Let’s connect to get you set up for long-term success.

🏠 If you’re a member of a younger generation, like Gen Z, you may be asking the question: will I ever be able to…

🏠 Thinking about selling your house? As you make your decision, consider what’s pushing you to think about moving Read more…

🏠 Thinking about selling your house? If you are, you might be weighing factors like today’s mortgageRead more…

🏠 Over the past year, many have discussed the challenge of buying a home. While affordability remains Read more…

🏠 Expenses involved in buying a home, from the down payment to closing costs. But did you know your tax refund can Read more…

🏠 If you’re dealing with student loans and considering homeownership, you might wonder how your debt influences your plans Read more…

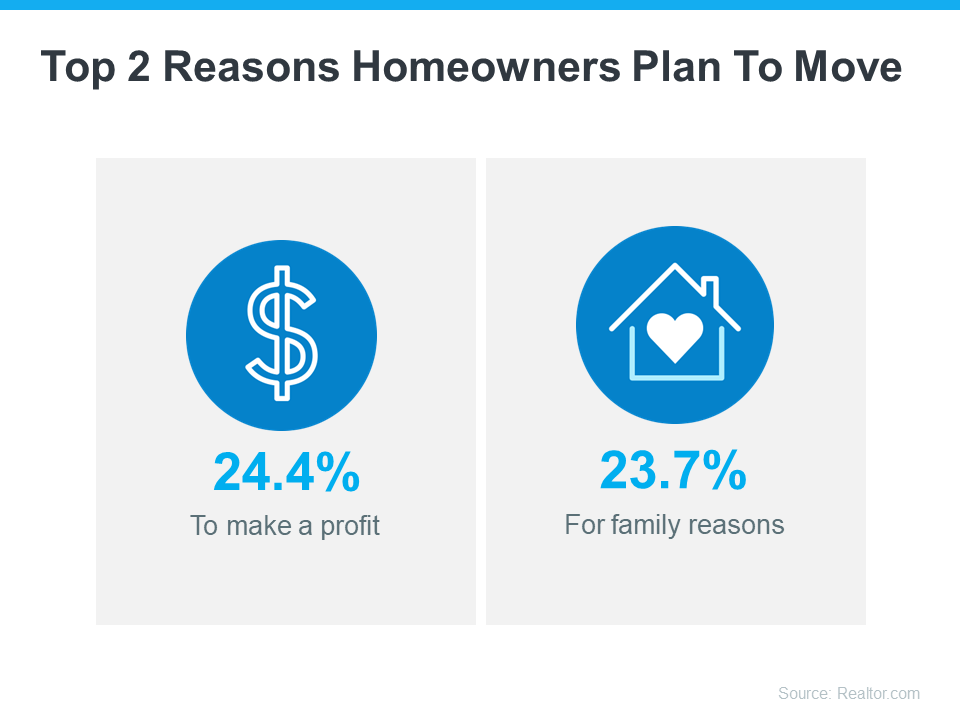

Thinking about selling your house? As you make your decision, consider what’s pushing you to think about moving. A recent survey from Realtor.com looked into why people want to sell their homes this year. Here are the top two reasons (see graphic below):

Let’s take a closer look and see if they’re motivating you to make a change too.

If you’re thinking about selling your house, you probably have a lot of questions on your mind. Well, here’s some good news – the latest data shows most sellers get a great return on their investment when they sell. ATTOM, a property data provider, explains:

“. . . home sellers made a $121,000 profit on the typical sale in 2023, generating a 56.5 percent return on investment.”

That’s significant. And here’s one contributing factor. During the pandemic, home prices skyrocketed. There was way more buyer demand than homes available for sale and that combination pushed prices up.

Now, home prices are still rising, just not as fast. That ongoing appreciation is good news for your bottom line. Any profit you make can help offset some of today’s affordability challenges when you buy your next home.

If you want to know how much your house is worth now and what’s going on with prices in your area, talk to a local real estate agent.

Maybe you want to be near relatives to help take care of older family members or to have more support nearby. Or maybe you’re just eager to spend time together on special occasions like birthdays and holidays.

Selling a house and moving closer to the people who matter the most to you helps keep you connected. If the distance is making you miss out on some big milestones in their lives, it might be time to talk to a local real estate agent to find a place close by. The National Association of Realtors (NAR) says:

“A great real estate agent will guide you through the home search with an unbiased eye, helping you meet your buying objectives while staying within your budget.”

If you’re thinking about selling your house, there’s probably a good reason for it. Let’s talk so you have help making the right move to reach your goals this year.

🏠 Thinking about selling your house? As you make your decision, consider what’s pushing you to think about moving Read more…

🏠 Thinking about selling your house? If you are, you might be weighing factors like today’s mortgageRead more…

🏠 Over the past year, many have discussed the challenge of buying a home. While affordability remains Read more…

🏠 Expenses involved in buying a home, from the down payment to closing costs. But did you know your tax refund can Read more…

🏠 If you’re dealing with student loans and considering homeownership, you might wonder how your debt influences your plans Read more…

🏠 Thinking of moving? It’s the perfect time to start. Experts recommend listing your house soon, as the best week for Read more…

Thinking about selling your house? If you are, you might be weighing factors like today’s mortgage rates and your own changing needs to figure out your next move.

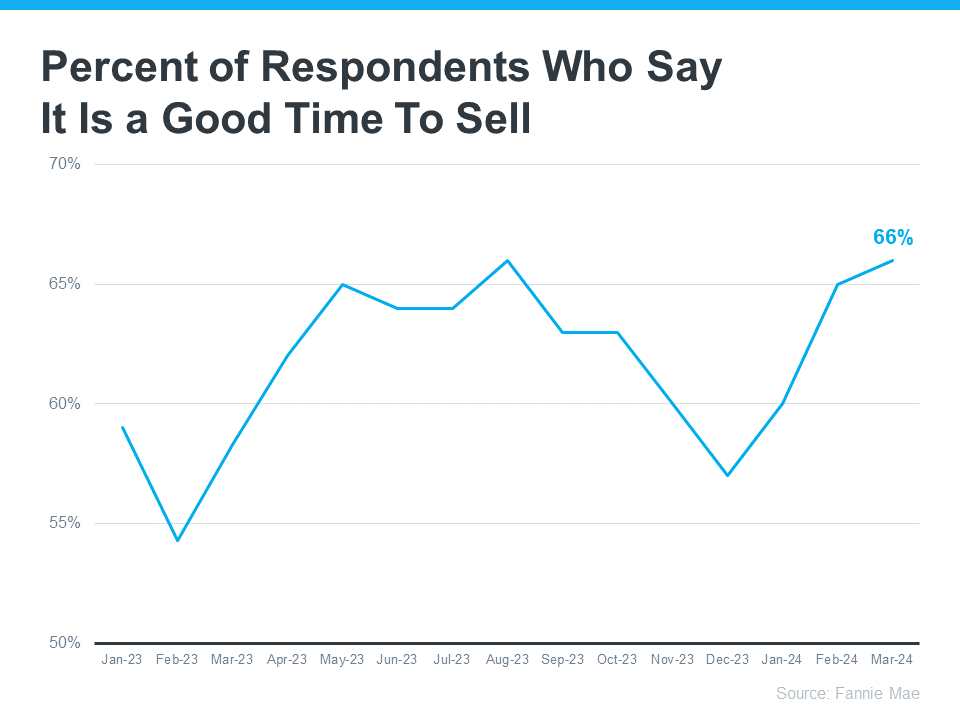

Here’s something else to consider. According to the latest Home Purchase Sentiment Index (HPSI) from Fannie Mae, the percent of respondents who say it’s a good time to sell is on the rise (see graph below):

One reason why is because right now is traditionally the best time of year to sell a house. A recent article from Bankrate says:

“Late spring and early summer are generally considered the best times to sell a house. . . . While today’s rates are relatively high, low inventory is still keeping sellers in the driver’s seat in most markets.”

These are the seasons when most people move. That means buyer demand grows. And because there still aren’t enough homes for sale to meet that demand, sellers see some serious perks. According to Rocket Mortgage:

“Homes that are listed at the end of spring and the beginning of summer typically sell faster at a higher sales price.”

More sellers are coming to realize conditions are ripe for a move. And that’s one reason why we’re seeing more homeowners put their homes up for sale. If you think you might want to get in on the action, it’s a good idea to start preparing.

A local real estate agent can help you get your house ready by offering advice on how best to fix it up and make it appealing to buyers in your area.

They also know if you list during the peak buying seasons of spring and early summer, you might sell quickly and for a higher price.

If you list during the spring and early summer, you might sell your house quickly and for a higher price. When you’re ready to make the most of today’s seller’s market, let’s get in touch.

🏠 Thinking about selling your house? If you are, you might be weighing factors like today’s mortgageRead more…

🏠 Over the past year, many have discussed the challenge of buying a home. While affordability remains Read more…

🏠 Expenses involved in buying a home, from the down payment to closing costs. But did you know your tax refund can Read more…

🏠 If you’re dealing with student loans and considering homeownership, you might wonder how your debt influences your plans Read more…

🏠 Thinking of moving? It’s the perfect time to start. Experts recommend listing your house soon, as the best week for Read more…

🏠 Thinking about buying a home? If so, you’re probably wondering: should I buy now or wait? Nobody can make that decision. Read more…

Over the past year or so, a lot of people have been talking about how tough it is to buy a home. And while there’s no arguing affordability is still tight, there are signs it’s starting to get a bit better and may improve even more throughout the year. Elijah de la Campa, Senior Economist at Redfin, says:

“We’re slowly climbing our way out of an affordability hole, but we have a long way to go. Rates have come down from their peak and are expected to fall again by the end of the year, which should make homebuying a little more affordable and incentivize buyers to come off the sidelines.”

Here’s a look at the latest data for the three biggest factors that affect home affordability: mortgage rates, home prices, and wages.

Mortgage rates have been volatile this year – bouncing around in the upper 6% to low 7% range. That’s still quite a bit higher than where they were a couple of years ago. But there is a sliver of good news.

Despite the recent volatility, rates are still lower than they were last fall when they reached nearly 8%. On top of that, most experts still think they’ll come down some over the course of the year. A recent article from Bright MLS explains:

“Expect rates to come down in the second half of 2024 but remain above 6% this year. Even a modest drop in rates will bring both more buyers and more sellers into the market.”

Any drop in rates can make a difference for you. When rates go down, you can afford the home you really want more easily because your monthly payment would be lower.

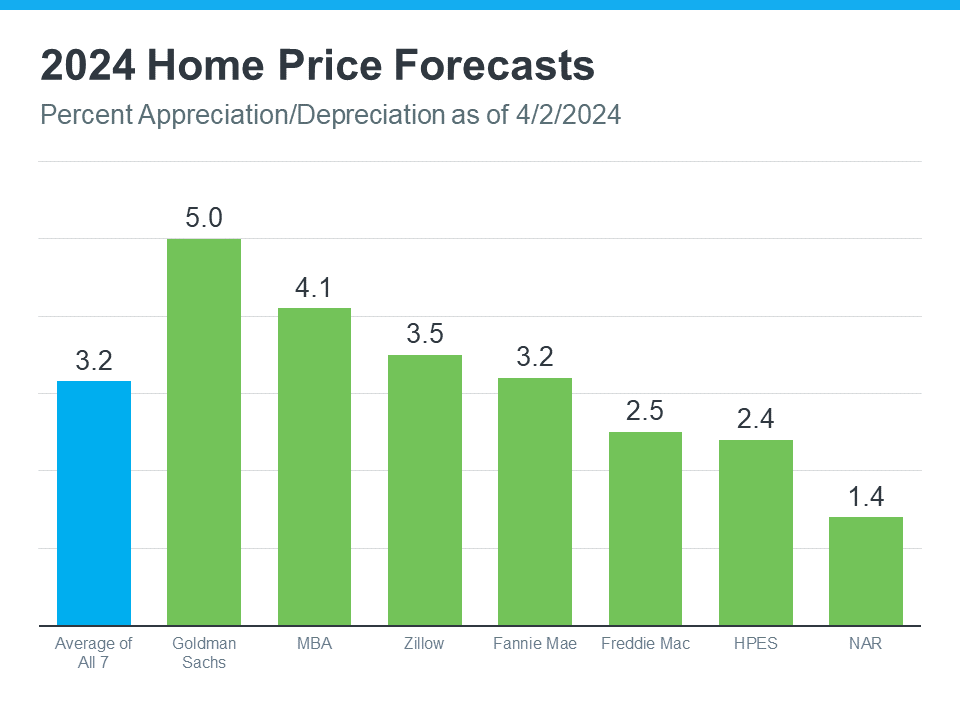

The second big factor to think about is home prices. Most experts project they’ll keep going up this year, but at a more normal pace. That’s because there are more homes on the market this year, but still not enough for everyone who wants to buy one. The graph below shows the latest 2024 home price forecasts from seven different organizations:

These forecasts are actually good news for you because it means the prices aren’t likely to shoot up sky high like they did during the pandemic. That doesn’t mean they’re going to fall – they’ll just rise at a slower pace.

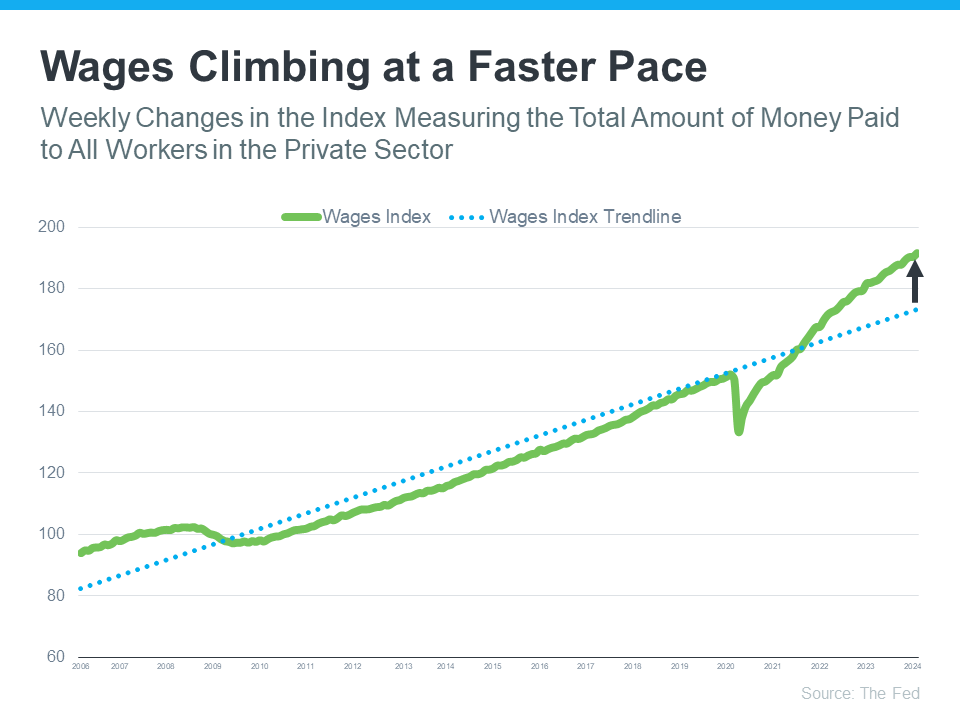

One factor helping affordability right now is the fact that wages are rising. The graph below uses data from the Federal Reserve to show how wages have been growing over time:

Check out the blue dotted line. That shows how wages typically rise. If you look at the right side of the graph, you’ll see wages are climbing even faster than normal right now.

Here’s how this helps you. If your income has increased, it’s easier to afford a home because you don’t have to spend as big of a percentage of your paycheck on your monthly mortgage payment.

If you stack these factors up, you’ll see mortgage rates are still projected to come down a bit later this year, home prices are going up at a more moderate pace, and wages are growing quicker than normal. Those trends are a good sign for your ability to afford a home.

🏠 Over the past year, many have discussed the challenge of buying a home. While affordability remains Read more…

🏠 Expenses involved in buying a home, from the down payment to closing costs. But did you know your tax refund can Read more…

🏠 If you’re dealing with student loans and considering homeownership, you might wonder how your debt influences your plans Read more…

🏠 Thinking of moving? It’s the perfect time to start. Experts recommend listing your house soon, as the best week for Read more…

🏠 Thinking about buying a home? If so, you’re probably wondering: should I buy now or wait? Nobody can make that decision. Read more…

🏠 Are you thinking about buying a home soon? If so, you should know today’s market is competitive in many areas because Read more…

Have you been saving up to buy a home this year? If so, you know there are a number of expenses involved – from your down payment to closing costs. But did you also know your tax refund can help you pay for some of these expenses? As Credit Karma explains:

“If one of your goals is to stop renting and buy a home, you’ll need to save up for closing costs and a down payment on the mortgage. A tax refund can give you a start on the road to homeownership. If you’ve already started to save, your tax refund could move you down the road faster.”

While how much money you may get in a tax refund is going to vary, it can be encouraging to have a general idea of what’s possible. Here’s what CNET has to say about the average increase people are seeing this year:

“The average refund size is up by 6.1%, from $2,903 for 2023’s tax season through March 24, to $3,081 for this season through March 22.”

Sounds great, right? Remember, your number is going to be different. But if you do get a refund, here are a few examples of how you can use it when buying a home. According to Freddie Mac:

The best way to get ready to buy a home is to work with a team of trusted real estate professionals who understand the process and what you’ll need to do to be ready to buy.

Your tax refund can help you reach your savings goal for buying a home. Let’s talk about what you’re looking for, because your home may be more within reach than you think.

🏠 Expenses involved in buying a home, from the down payment to closing costs. But did you know your tax refund can Read more…

🏠 If you’re dealing with student loans and considering homeownership, you might wonder how your debt influences your plans Read more…

🏠 Thinking of moving? It’s the perfect time to start. Experts recommend listing your house soon, as the best week for Read more…

🏠 Thinking about buying a home? If so, you’re probably wondering: should I buy now or wait? Nobody can make that decision. Read more…

🏠 Are you thinking about buying a home soon? If so, you should know today’s market is competitive in many areas because Read more…

🏠 If you’re trying to buy a home and are having a hard time finding one you can afford, it may be time to…

REALTOR®

707.816.0922

ashleycruzhomes@gmail.com

DRE Lic# 02126949

Made with ❤️ by navi © 2024